26 companies

Credits & Loans

...

Experiences with Credits & Loans

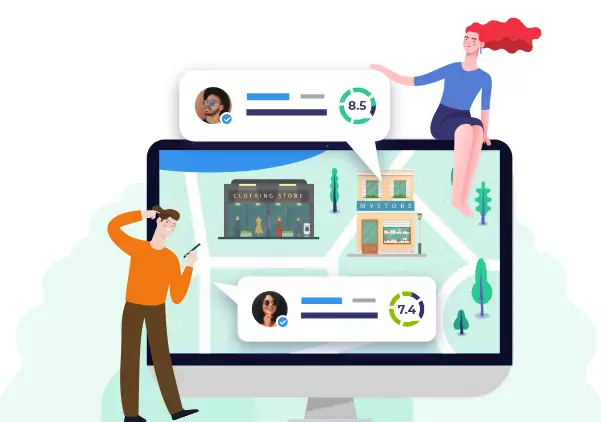

Navigating the world of credits and loans involves finding the right fit for your financial needs, whether it’s a personal loan, mortgage, or credit line. Key concerns include understanding interest rates, hidden fees, and repayment terms—pitfalls like adjustable rates can lead to unexpected payments. For instance, a variable interest rate might seem low initially, but can significantly increase your monthly dues over time. Explore the reviews and compare companies on this page to ensure informed decisions, and consider sharing your experiences to help others.

Companies

24 reviews

24 reviews

20 reviews

1 reviews

21 reviews

22 reviews

20 reviews

18 reviews

26 reviews

8 reviews

18 reviews

1 reviews

8 reviews

7 reviews

9 reviews

10 reviews

4 reviews

13 reviews

2 reviews

6 reviews

5 reviews

8 reviews